When should you start planning for retirement? Ask a financial expert, and you’ll likely get the same answer every time — as soon as you start your career. However, it’s never too late to start retirement planning.

Retirement planning is a crucial component of financial stability, offering peace of mind that you can maintain your quality of life and independence long after you’ve left the workforce. Whether you are just starting your career, are in the thick of it, or are preparing to retire, there are strategic steps you can take at each stage to secure your financial future. This guide, with information from financial planners at Ernst & Young and NerdWallet, provides an in-depth look at effective retirement strategies tailored to different career stages.

Understanding the importance of retirement planning

Retirement planning is vital because it ensures that you have the resources to maintain your lifestyle even when regular paychecks stop. It allows for financial independence and the freedom to enjoy your later years without significant financial constraints. For many, the reality of Social Security means it may not fully cover all expenses or match the income they were accustomed to while working. This underscores the need for a well-rounded and proactive approach to retirement planning.

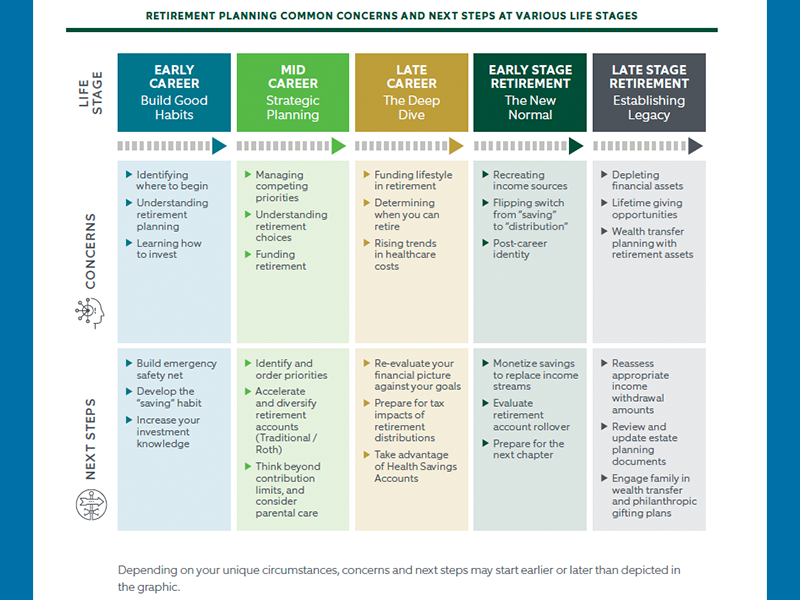

Early career: Establishing a solid foundation

The foundation of your retirement planning should be laid early in your career. This stage is all about setting habits that will pay off in the future.

Strategic steps for early career planning:

- Begin saving immediately: The power of compound interest means that the earlier you start saving, the more you will accumulate. Utilize any available employer retirement plans, especially those that offer matching contributions, to maximize your savings.

- Invest wisely: Understand the basics of investing and choose options that align with your long-term goals and risk tolerance. Younger professionals have the advantage of time, allowing them to recover from market fluctuations and benefit from higher-risk, higher-return investments.

- Regular portfolio reviews: Make adjustments to your investments based on changes in your life circumstances and financial goals. This proactive approach helps keep your retirement plan on track.

- Benefits of Starting Early: Starting your retirement savings early uses time as your greatest asset. Compounding allows your investments to grow exponentially over the years, making it easier to achieve substantial retirement savings.

Mid-career: Accelerating retirement savings

As you move into your mid-career, you typically enjoy higher earnings and potentially more financial stability. This is the primary time to boost your retirement savings.

Key strategies for mid-career:

- Maximize contributions: Take full advantage of your peak earning years by maximizing your contributions to various retirement accounts. This not only includes 401(k)s and IRAs but also exploring other investment opportunities.

- Reevaluate investment strategies: This is an ideal time to assess whether your current investment mix matches your risk tolerance and retirement timeline. It might be appropriate to start diversifying your investments to include a mix of growth and income-focused assets.

- Take advantage of employer benefits: Fully explore and utilize all employer-provided benefits, which can include stock options, additional matching, or other financial planning services.

Late career: Preparing for the transition

In the late stages of your career, the focus shifts towards preparing for the transition into retirement. This includes making strategic choices about when to retire and how to manage your investments and income sources.

Strategic planning for late career:

- Catch-up contributions: Individuals over 50 can make additional contributions to their retirement accounts, significantly boosting retirement funds.

- Conservative investment shift: Begin transitioning your investment strategy from growth-focused to more conservative, income-producing assets. This helps protect your savings from market volatility as you approach retirement.

- Income planning: Develop a clear plan for how you will convert your retirement savings into a steady stream of income. Consider factors like Social Security timing, pension distributions, and whether part-time work or other income sources are desirable.

Retirement income strategies

Understanding how to manage your income sources in retirement is critical. This might include deciding between lump-sum payouts and annuities, determining the optimal time to start taking Social Security benefits, and planning for required minimum distributions from retirement accounts. Effective retirement planning involves several steps that should be tailored to your individual financial situation and goals:

- Determine your retirement needs: Assess how much money you will need annually to maintain your desired lifestyle in retirement. Consider factors like health care costs, travel plans, and ongoing living expenses.

- Prioritize financial goals: While retirement savings should be a priority, it’s also important to balance this with other financial commitments, such as college savings for children or paying down high-interest debt.

- Select the right retirement accounts: Depending on your employment situation, this might include traditional and Roth IRAs, 401(k)s, or self-employed plans like SEP IRAs or Solo 401(k)s.

- Investment selection: Choose investments that fit your risk tolerance and retirement timeline. A diversified portfolio can help manage risk and provide growth opportunities.

Regular review and adjustment: Your financial situation and the economic environment will change over time. Regularly reviewing and adjusting your retirement plan ensures it remains aligned with your goals.

Retirement planning across different age groups

Understanding how you compare to your peers can be motivating. However, it’s important to focus on personalized goals rather than just averages.

The average retirement age has gradually increased from 57 in 1991 to 62 in 2024, reflecting changes in economic conditions, life expectancy, and shifts in Social Security benefits. Additionally, economic challenges like the Great Recession and the COVID-19 pandemic have led many to delay retirement.

Further, claiming Social Security too early reduces benefits, whereas delaying benefits can increase them. Full retirement age varies by birth year but is generally around 67. Medicare eligibility begins at 65, but planning for health care costs in retirement should start earlier.

Penalty-free withdrawals from retirement accounts like 401(k)s and IRAs start at 59½, with specific exceptions allowing earlier access. Roth IRA contributions can be withdrawn tax-free at any time, offering flexible financial planning options.

According to data from the Federal Reserve’s 2022 Survey of Consumer Finances, retirement savings by age group are as follows:

- Under 35: Average savings of $49,130 and median of $18,880; about 50% have retirement accounts.

- 35-44: Average savings of $141,520 and median of $45,000; nearly 62% have retirement accounts.

- 45-54: Average savings of $313,220 and median of $115,000; about 62% have retirement accounts.

- 55-64: Average savings of $537,560 and median of $185,000; around 57% have retirement accounts.

- 65-74: Average savings of $609,230 and median of $200,000; about 51% have retirement accounts.

These figures highlight the progression of savings with age, influenced by factors like increased earnings, compound interest, and investment maturity. However, many Americans are not saving enough, with significant gaps between average and median savings indicating wide disparities.

Effective retirement planning is essential for a secure and enjoyable retirement. It requires adapting to life changes and economic conditions through strategic saving, investing, and planning. By understanding and applying tailored strategies at each career stage — and considering personal circumstances rather than just averages — you can build a robust financial foundation for the future.

Whether you’re just starting out, in the thick of your career, or nearing your retirement, proactive management of your retirement planning will pave the way for a comfortable and fulfilling retirement.

The future of Social Security and Medicare

As the United States faces an aging population and a rising federal debt, the solvency of Social Security and Medicare becomes an increasingly urgent issue. Recent reports indicate that without significant intervention, Social Security and Medicare could face insolvency within the next decade, raising concerns about the sustainability of benefits for millions of Americans.

Solvency projections

According to a recent Washington Post report, these programs are fundamental to the financial security of seniors, yet they are projected to run out of money due to demographic shifts and financial pressures. A robust job market has temporarily improved the financial outlook for these programs, as “the low unemployment rate means more workers are contributing to the programs.” However, this is only a temporary reprieve within an overall bleak fiscal picture.

Congressional action needed

The urgency to act is compounded by the imminent risk of these programs facing cuts. 2025 will be filled with unavoidably huge fiscal moments, and addressing the solvency of Social Security and Medicare should be at the forefront of these considerations. Despite the pressing need, significant political challenges complicate efforts to reform these vital programs. Neither recent administrations nor current lawmakers have presented a viable plan to secure their financial future.

Proposed solutions

Debates over how to stabilize these programs center around a few key proposals:

- Tax increases: Some propose increasing taxes on higher earners to boost the Social Security Trust Fund. President Biden has suggested raising taxes on individuals earning more than $400,000 to support Social Security.

- Benefit cuts: Conversely, some policymakers have considered cuts to benefits, including raising the retirement age. However, this approach is highly contentious and seen as a political third rail.

- Privatization proposals: Past proposals, such as President George W. Bush’s idea to allow private retirement accounts, have met with strong opposition, highlighting the political sensitivity of reforming Social Security.

The economic implications

The failure to address the fiscal challenges facing Social Security and Medicare not only threatens the financial well-being of millions of Americans but also has broader economic implications. The potential increase in federal borrowing needed to cover benefits could explode the federal debt and trigger larger economic consequences. As borrowing costs rise, they could outpace economic growth, leading to a cycle of ever-increasing debt.

The need for urgent reform

As the “silver tsunami” of retiring baby boomers places increasing pressure on these programs, the window for effective reform narrows. The growing anxiety among current and future retirees underscores the critical nature of these discussions.

The challenges facing Social Security and Medicare are emblematic of larger issues in federal fiscal policy, necessitating courageous and innovative solutions from our leaders. The need for reform is clear, and the consequences of inaction could be severe, impacting not just today’s seniors but future generations as well.